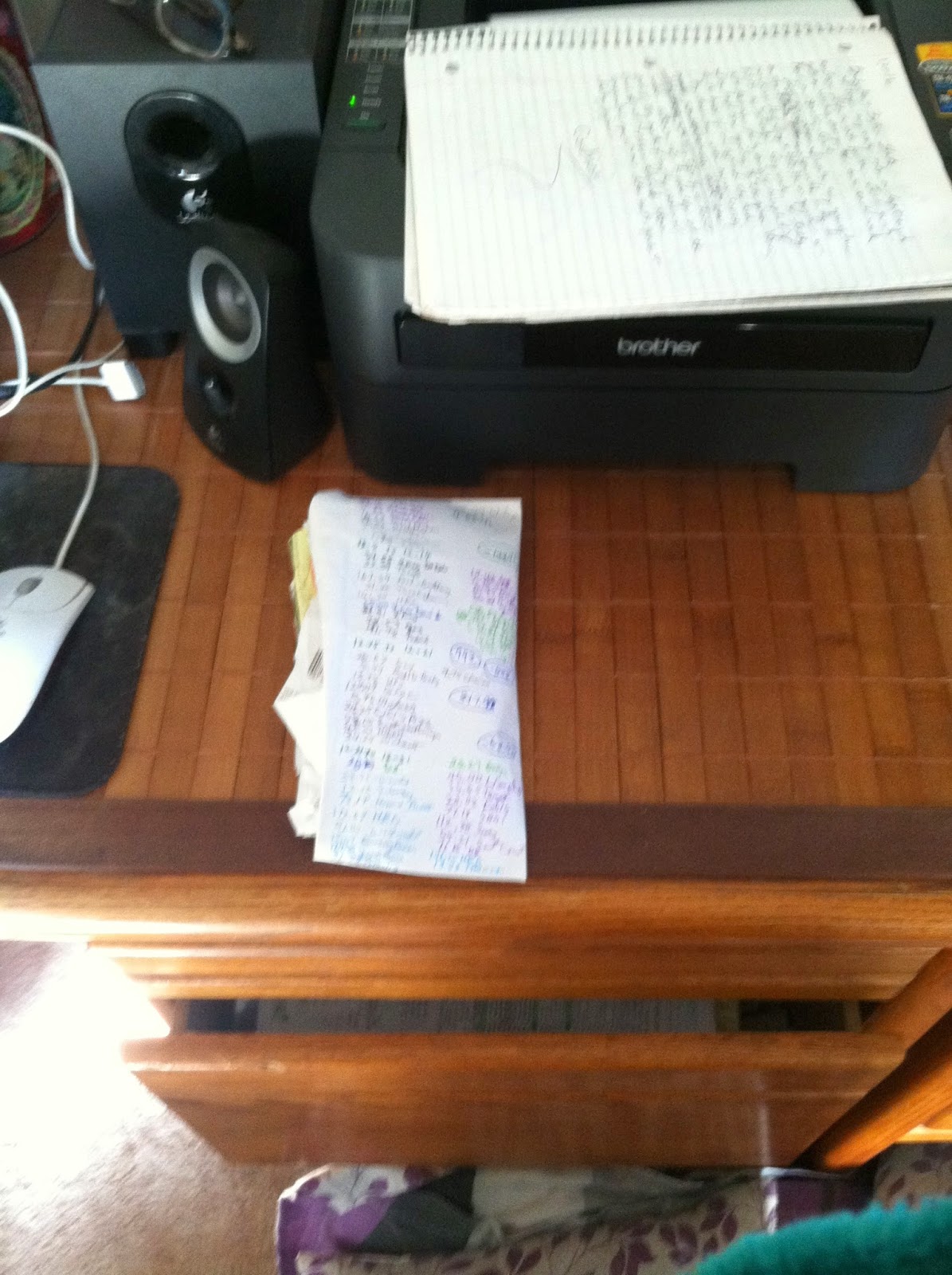

I begin every month with taking a

legal sized envelope and folding it into fourths. Each quarter gets a week’s

designation, and each week receives a spending limit. I record all expenditures

on the virgin exterior of the envelope—whether it be a major outflow like

$142.15 for groceries or something as minor as $3.14 for a Sonic Slush. At the

end of every week, I total the damage, feeling smugly triumphant if I’ve kept

our spending in the green, or vowing to do better if we dip into the red. My

obsession with number crunching allows us to indulge at the end of the month if

anything extra remains. Most of the time, though, we simply break even. By the

end of each month, the overstuffed envelope’s surface is covered with numbers

and notes on spending habits. It remains in my upper desk drawer until the

credit card statement arrives as a means of double checking the balance for our

month’s expenses.

I begin every month with taking a

legal sized envelope and folding it into fourths. Each quarter gets a week’s

designation, and each week receives a spending limit. I record all expenditures

on the virgin exterior of the envelope—whether it be a major outflow like

$142.15 for groceries or something as minor as $3.14 for a Sonic Slush. At the

end of every week, I total the damage, feeling smugly triumphant if I’ve kept

our spending in the green, or vowing to do better if we dip into the red. My

obsession with number crunching allows us to indulge at the end of the month if

anything extra remains. Most of the time, though, we simply break even. By the

end of each month, the overstuffed envelope’s surface is covered with numbers

and notes on spending habits. It remains in my upper desk drawer until the

credit card statement arrives as a means of double checking the balance for our

month’s expenses.

My obsession continues into my

record keeping. I have ledgers dating back to those first months of our

marriage where we stretched $850 a month income across apartment rent,

utilities, insurance, school loans and food. The numbers may have changed over

the years, but my strategy remains the same. I know exactly where every penny

goes, can use one year’s budget to project into the next year, and based on one

year’s spending will plan financial goals.

I rarely set the goal of saving

money just to save it. We don’t have some huge balance accruing that hasn’t

been assigned an end purpose. The chunk of money accumulating in our Money

Market goes to taxes on our home this month and anything left over will stay in

place for April’s income taxes and work on the car. All of the budgeting and

balance sheets pays off in the long run. We work together as a family to reach

very specific spending goals. By watching the outflow carefully, we’ve plugged

up leaks and pooled funds into building a secure future.

Sometimes I wonder if I’d hold onto

the monthly envelope and colorful ledgers if our income ever rose. Would I stop

tracking that dollar spent here? Or that five spent over there? Then I admit

with chagrin that number crunching flows through my veins. It’s part of who I

am, how I think. Whether I have only a teacher’s retirement income or a million

dollars doesn’t matter. I’d track my spending, set my goals, and record all

expenditures.

Maybe I’d just have a larger

envelope!

Copyright 20214 Elizabeth Abrams Chapman

This is a good idea. I have tried tracking bills, payments and expenditures, but it is quite a task. I fall behind and try to start over. Maybe one of these days I will keep on top of it. Good job and good planning.

ReplyDelete